Client Portal

Get a Quote

UA is committed to collaborating with and assisting our clients to achieve and surpass their financial goals. If you're considering your next move, be sure to contact us today!

X

Global markets moved higher over the September quarter as confidence grew in a soft landing for major economies and a gradual shift towards monetary easing. Easing inflation pressures and more balanced central bank messaging supported sentiment, while volatility remained subdued. Overall, risk appetite improved as investors became more optimistic about the outlook for growth and policy settings heading into year end.

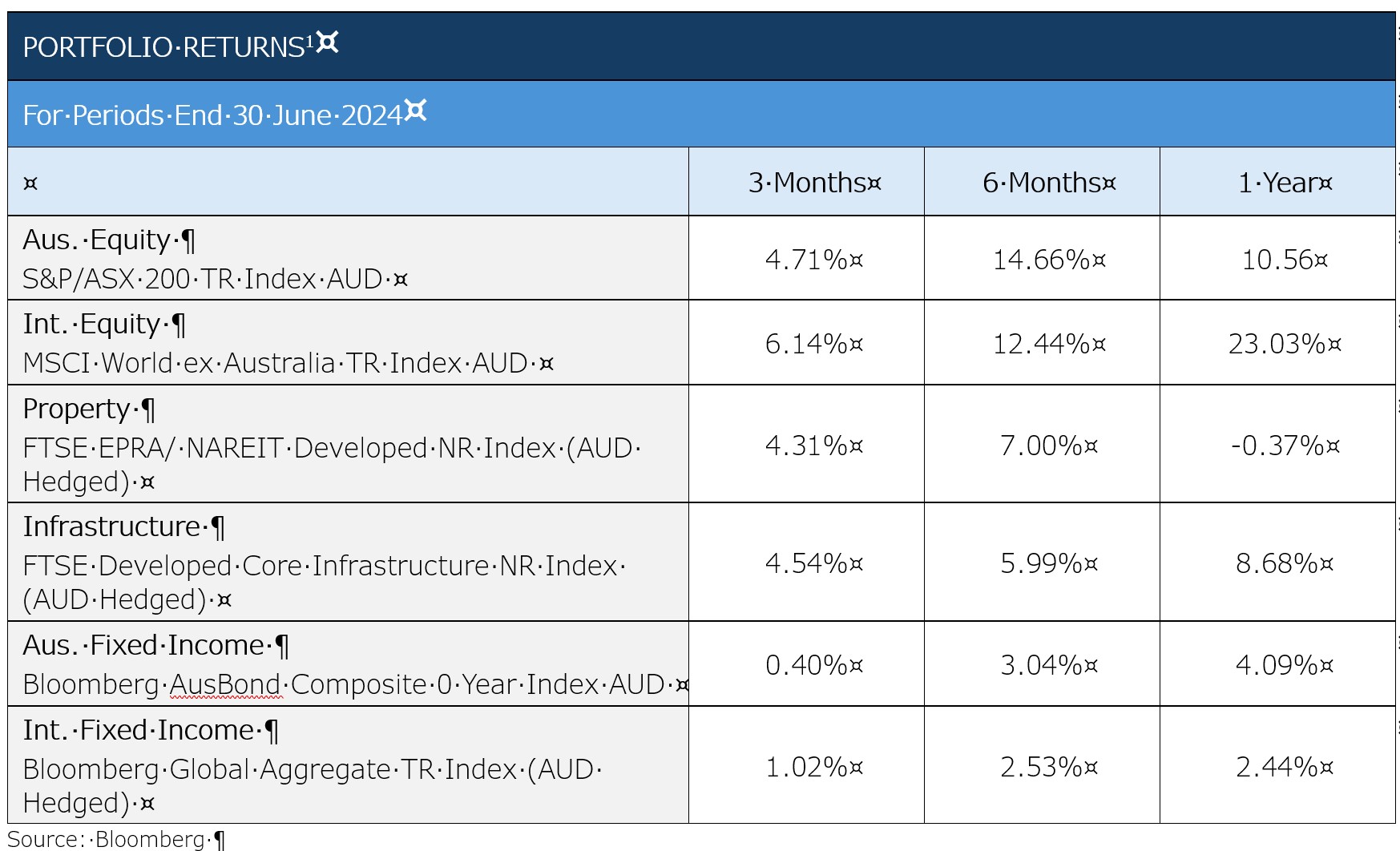

Australian Equities

The ASX 200recorded its 2nd quarterly gain for the year, rising through a period that provided a volatile reporting season as well as an improving investor sentiment as inflation looked to stabilise before a slightly concerning monthly print.

Australian Equities rose 4.71% across the quarter with Materials the best performer+18.65%, followed by Utilities +9.5% and Consumer Discretionary +9.06%. The main laggards were Healthcare which suffered from a slew of poor earnings, falling -10.06% across the quarter, while Energy continued its poor year -3.95%and Consumer Staples rounded out the 3 sectors in negative territory falling-3.09%.

At the stock level, DroneShield (DRO) was the standout performer, surging 104.4% after delivering a strong earnings result and announcing new contract wins in defence technology. The weakest performer was Boss Energy (BOE), which fell -55.9% amid weaker uranium prices and production delays at its Honeymoon project.

International Equities

The MSCI World ex‑Australia Total Return Index(AUD) rose 5.94% in the September quarter, supported by an easing bias from the US Federal Reserve Bank, signs of a cooling US labour market, and lower bond yields that boosted risk assets.

US equities led the gains, with the S&P 500up 7.04%, the Nasdaq rising 8.07%, and small caps outperforming, as the Russell2000 climbed 11.24%. Europe also contributed positively, with the Euro Stoxx up3.11% and the FTSE 100 gaining 4.02%.

Technology and AI‑linked names, alongside resilient corporate earnings, drove broader participation, helping offset ongoing geopolitical and inflationary uncertainties.

Real Assets

Listed infrastructure had a strong quarter, delivering 4.54% in AUD-hedged terms while listed property was similarly strong, rising 4.31% in AUD-hedged terms.

Fixed Income

Bond returns were positive but lagging their varying asset classes as global yield curves drifted lower over the course of the quarter, with the majority of the move in September as the potential of a US government shutdown loomed. The Bloomberg AusBond Composite up 0.4% and the Bloomberg Global Aggregate (AUD-hedged) up1.02%.

Currency Markets

The U.S. Dollar Index (DXY) rose by 0.93% over the quarter to about 97.77, its first positive quarter for the year, as markets re-priced a potential September Fed cut to no cut. The AUD was also positive as rate expectations shifted locally, finishing+0.49%, at 66.13c, up from 65.81c.

Commodities

Commodities were mixed over the month with oil falling for a 2nd consecutive quarter, down 0.87%, while gold (+16.83%) and silver (+29.18%) surged.

Important Information: This content is issued by Mason Stevens Asset Management Pty Limited, ABN 92 141 447 654 (MSAM).MSAM is a corporate authorised representative (CAR 461312) of Mason Stevens Limited, ABN 91 141 447207, AFSL 351578 (Mason Stevens). The information provided is of a general nature only and does not have regard to any individual’s personal objectives, financial situation, or needs. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. MSAM encourages seeking specific professional advice from a licensed financial adviser before making a decision to transact in relation to any investment, security, or strategy. Investment in securities including derivatives involves risks. Securities by nature will rise and fall and therefore past performance is not a reliable indicator of future performance. MSAM and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained inthis communication. MSAM ensures that the information provided in this communication is as accurate and complete as possible but does not warrant itsaccuracy or reliability. References made to any third party, or their data is based on information that Mason Stevens believes to be true and accurate asat the date of this communication but is without independent verification. Opinions and or information may change without notice and Mason Stevens isnot obliged to update you if the information changes. Mason Stevens and its associated companies, authorised representatives, agents, and employeesexclude to the full extent by law, liability of whatever kind, including negligence, contract, fiduciary duties or otherwise, to investors or anyone else inrespect of any loss or damage, including indirect or consequential loss or damage, foreseeable or not, arising from or in connection with this information.

UA is committed to collaborating with and assisting our clients to achieve and surpass their financial goals. If you're considering your next move, be sure to contact us today!

X